Bank Test Rates Explained: The Hidden Factor Behind Your Borrowing Power

Banks assess your mortgage using a higher “test rate” — not your actual interest rate — which directly impacts how much you can borrow.

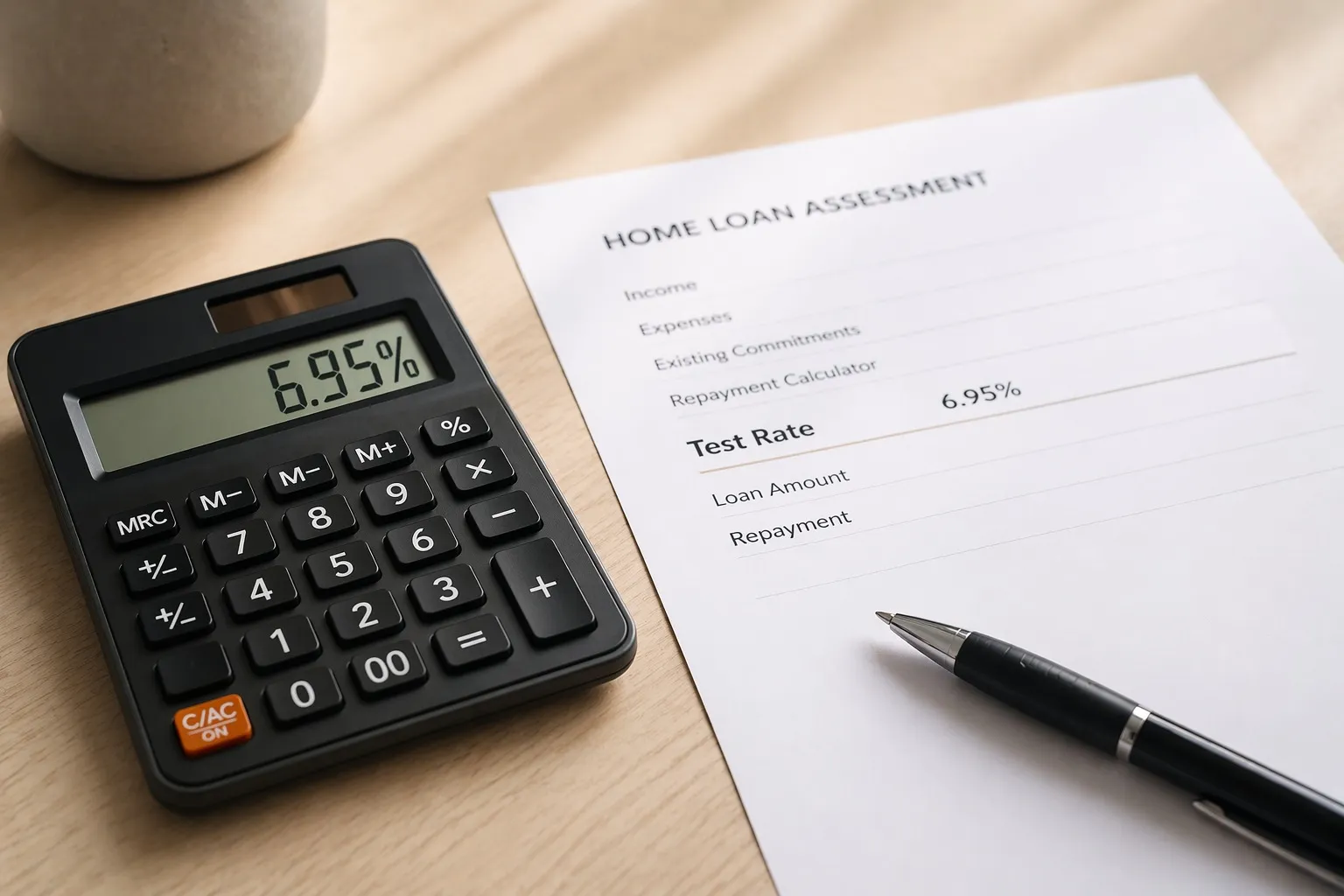

What Is a Bank Test Rate?

A test rate is the interest rate banks use to assess your affordability — not your actual repayments.

Right now, test rates are typically around 2.5% to 2.75% higher than the fixed rates being offered.

So even if you secure a rate in the 5% range, the bank may assess your loan closer to 6.5%–7%+.

What Happens When Interest Rates Increase?

When interest rates rise, banks typically increase their test rates as well.

This can have a direct impact on your borrowing power:

You may qualify for less lending

Your application may become tighter on affordability

In some cases, it can be the difference between approval and decline

Even small changes can make a noticeable difference.

Example: What a 0.25% Increase Does

Let’s look at a simple example.

Loan Amount: $600,000

Term: 30 years

Borrowing Power Comparison

Test Rate | Estimated Borrowing Power | Monthly Repayment (Assessment) |

|---|---|---|

6.70% | $600,000 | ~$3,870 |

6.95% | $600,000 | ~$3,972 |

Even though the repayment the bank is testing stays roughly the same, a higher test rate means the bank has to reduce the loan amount to keep it affordable.

In this example:

A 0.25% increase in the test rate reduces borrowing power by roughly $15,000

A 0.50% increase in the test rate can reduce borrowing power by roughly $25,000–$30,000

A 0.25% increase in test rates can reduce borrowing power by roughly $2,000–$3,000 per $100,000 of lending

A 0.50% increase in test rates can reduce borrowing power by roughly $4,000–$6,000 per $100,000 of lending

What This Means for You

Test rates are one of the biggest factors affecting your borrowing power — and they can change without you doing anything.

This means:

Your borrowing position can shift as rates move

Timing can play a role in how much you can borrow

Structuring your lending correctly becomes more important

Final Thoughts

You’re not assessed on today’s interest rate — you’re assessed on a higher “what if” rate.

That’s why two people on the same income can get very different results depending on when they apply.

If you’re thinking about buying, it’s worth understanding where test rates currently sit and how they may impact your position. Each bank generally has a different "test rate" so what you can potentially borrow may differ from bank to bank.

Need Help?

If you're not sure about your next steps or what you might qualify for, flick me a message.

I'll help you figure out your options, and guide you through the process.

Keep up with the latest mortgage updates:

Disclosure

Jason Bruce Mortgages is a licensed Financial Advice Provider (FAP), authorised by the Financial Markets Authority (FMA) to provide financial advice services. Group FSP Number: 1009241. Adviser: Jason Bruce (FSP Number: 669431). The information in this article is general in nature and is not personalised financial advice. Before you act on it, you should seek advice that is specific to your circumstances.

Under the Financial Markets Conduct Act, we must prioritise your interests, act with care, diligence, and skill, and meet ethical standards and appropriate client care.