The Hidden Deal Breakers in Your Bank Statements

Account conduct is one of the most common reasons a mortgage application is delayed, queried, or declined despite having sufficient income and deposit.

If you've watched my video on account conduct and want to learn more, this article breaks down what account conduct is, why banks pay so much attention to it, and some of the most common issues I see when assessing home loan applications.

What Is Account Conduct?

Account conduct is simply the way you manage your money on a day-to-day basis.

When a bank reviews your application, they're not just looking at your income, deposit, and expenses. They're also looking at how you operate your accounts and whether your financial commitments are being met consistently.

Checks Lenders look for:

Are your bills being paid on time?

Are direct debits and automatic payments being met?

Are accounts going into unarranged overdraft?

Are loan and credit card repayments being made when due?

Are there any dishonoured payments?

Are you spending money before important commitments are due?

Good account conduct demonstrates that you can manage your financial commitments effectively and consistently. Poor account conduct can raise concerns, even when income and affordability appear strong. Lenders want to see that commitments are being met on time and that your day-to-day banking habits support responsible financial management.

Unarranged Overdrafts

An unarranged overdraft occurs when a payment takes your account into a negative balance without an approved overdraft facility.

For example:

You have $30 in your account and a gym membership payment of $50 comes out. Your account temporarily goes to -$20 until you transfer money back in a day later.

At the end of the month, the bank may charge an unarranged overdraft fee.

What Does This Tell The Bank?

If it happens once during the three-month period a bank reviews, it's generally viewed as a one-off mistake and is easy to explain.

However, if it happens regularly, it can indicate one of two things:

Money management may not be as organised as it could be.

There may not be enough surplus cash available to comfortably meet existing commitments.

A common example I see is someone getting paid, immediately transferring money into savings, and then having a direct debit bounce the following day.

The positive is that they clearly have money available. The concern is that the account wasn't managed in a way that allowed all commitments to be met.

How To Fix It

Review your savings amount and ensure enough funds remain available to cover upcoming payments.

Saving slightly less while consistently meeting your commitments is generally far better than saving aggressively and incurring overdraft fees or missed payments.

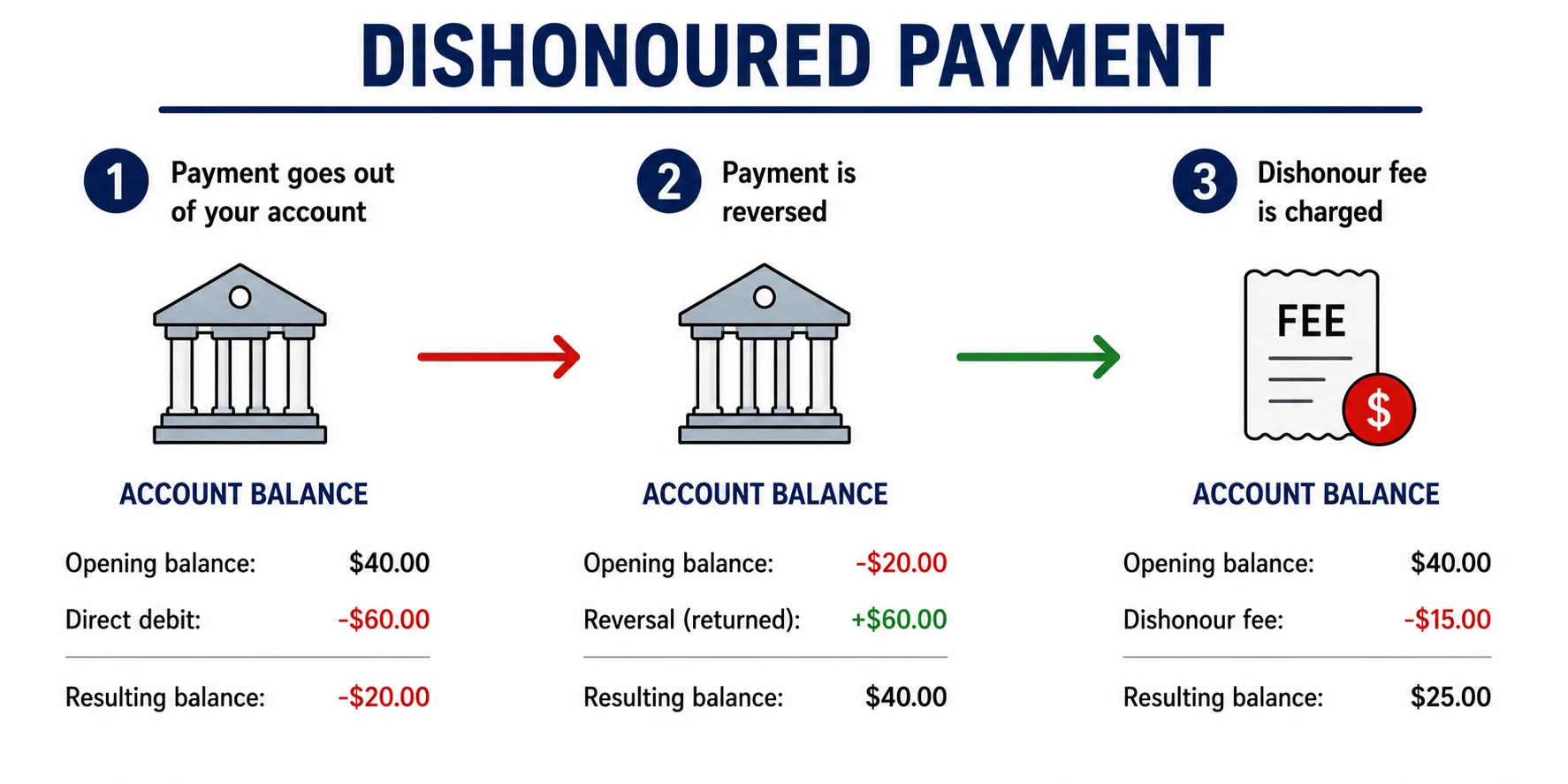

Dishonoured Direct Debits

A dishonoured direct debit occurs when a scheduled payment attempts to come out of your account but there aren't enough funds available.

On your statement, you'll often see the payment leave the account and then immediately reverse back in.

Common examples include:

Rent payments

Utility bills

Gym memberships

Insurance premiums

Subscription services

What Does This Tell The Bank?

Banks may question whether committed expenses are being prioritised appropriately.

For example, if someone is regularly spending money on discretionary items such as takeaways, entertainment, or shopping, but then doesn't have enough money available for committed payments, it can raise concerns around financial management.

Again, a one-off dishonour is usually easy to explain.

A pattern of dishonoured payments is where concerns begin to arise.

How To Fix It

The easiest solution is to align direct debits with your pay cycle.

Where possible:

Have wages paid into your account first.

Schedule direct debits for the following day.

Ensure committed expenses are covered before discretionary spending.

A simple adjustment to payment timing can often eliminate the problem completely.

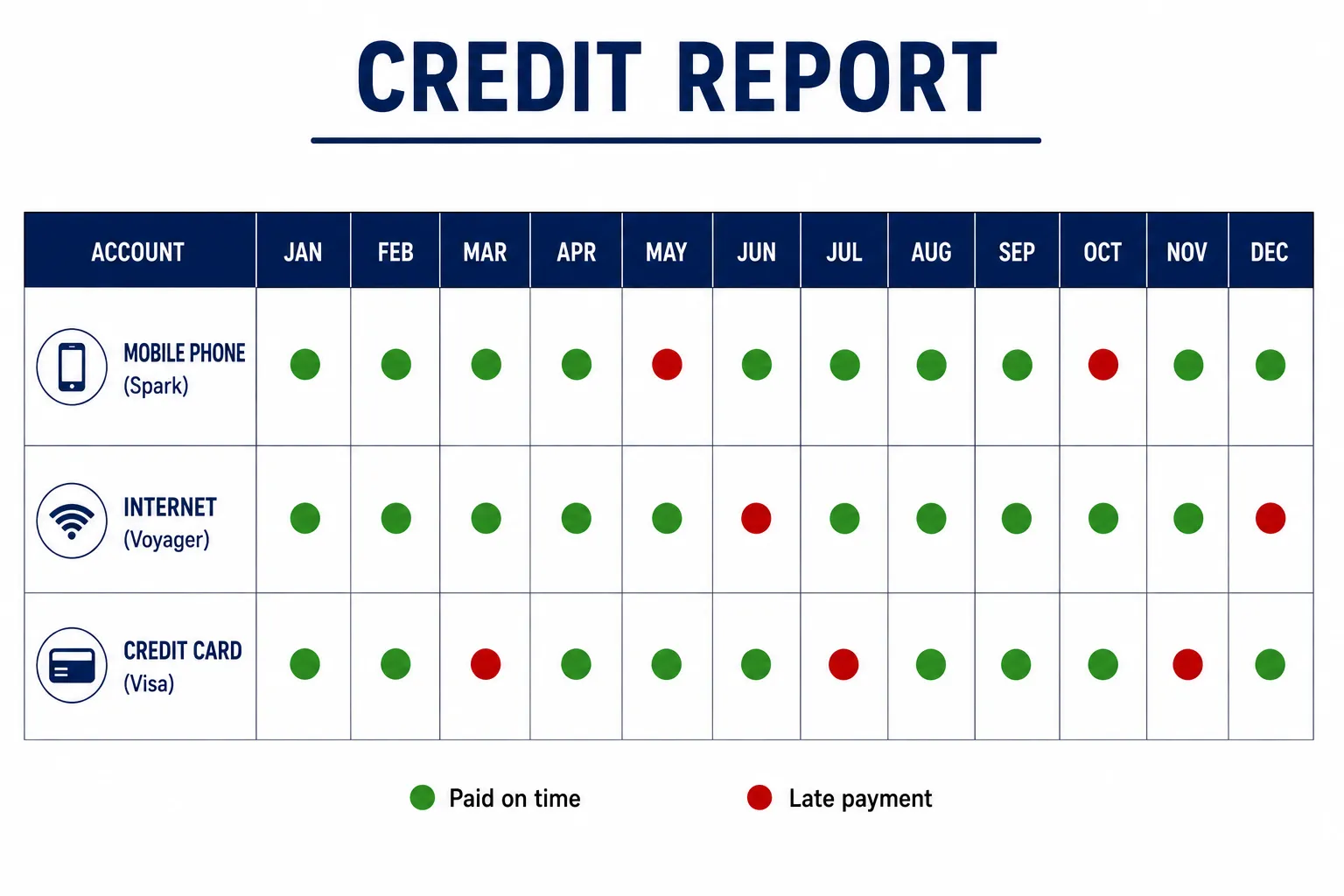

Late Payments To Utility Providers And Existing Credit Facilities

Another common issue is making payments late to utility providers or existing lending facilities.

Examples include:

Phone accounts

Internet providers

Power providers

Credit cards

Store cards

Personal loans

While an occasional late payment may not create significant concern, a pattern of late payments can become problematic.

Why Does This Matter?

Consistently paying accounts late can indicate financial pressure or poor account management.

In some cases, it can also negatively impact your credit score, making future lending applications more difficult.

From a lender's perspective, if existing commitments aren't being met on time, they may question how a new mortgage commitment will be managed.

How To Fix It

Set up automatic payments where possible and ensure due dates align with your income cycle.

Creating a system that allows bills to be paid automatically often removes the risk of missed or late payments altogether.

Common Account Conduct Red Flags

Some of the most common account conduct issues banks identify include:

Frequent unarranged overdrafts

Dishonoured direct debits

Repeated late bill payments

Excessive gambling transactions

Regular use of Buy Now Pay Later facilities

Cash advances on credit cards

Missed loan repayments

Not every item on this list will automatically result in a declined application. However, repeated patterns can create concerns and often lead to additional questions from the bank.

Why Account Conduct Matters

When assessing a mortgage application, banks assess both your ability and your willingness to repay debt.

This includes:

Income

Deposit

Existing debts

Living expenses

Account conduct

Your bank statements provide a real-life snapshot of how you manage money.

Good account conduct gives lenders confidence. Poor account conduct can result in additional questions, delays, or in some cases, a declined application.

Get Advice Early

One of the biggest mistakes I see is people engaging with a mortgage adviser too late in the process.

Account conduct is something that often takes time to demonstrate. In many cases, lenders want to see a consistent pattern over a three-month period.

If there are issues with your statements, an adviser may recommend spending a few months tidying things up before applying.

The good news is that if you get advice early, you'll know exactly what needs attention and can work on it before you're ready to purchase.

Most importantly, improving your account conduct doesn't just help with getting a mortgage. It can also save you money, reduce fees, improve your financial habits, and put you in a stronger position long term.

If you're unsure how your accounts would look to a lender, reach out for a review. A quick fact-check today could save you months down the track.

Need Help?

If you're not sure about your next steps or what you might qualify for, flick me a message.

I'll help you figure out your options, and guide you through the process.

Keep up with the latest mortgage updates:

Disclosure

Jason Bruce Mortgages is a licensed Financial Advice Provider (FAP), authorised by the Financial Markets Authority (FMA) to provide financial advice services. Group FSP Number: 1009241. Adviser: Jason Bruce (FSP Number: 669431). The information in this article is general in nature and is not personalised financial advice. Before you act on it, you should seek advice that is specific to your circumstances.

Under the Financial Markets Conduct Act, we must prioritise your interests, act with care, diligence, and skill, and meet ethical standards and appropriate client care.